Budgeting 101: Saving to Buy Your First House

Buying a home is the largest purchase many people will make during their lifetime, so it’s important to have a clear idea of how you are going to pay for the home. Budgeting for your first home means saving enough for the down payment and other purchase costs, but also budgeting for life after you make the big move.

Planning for a Down Payment

Though it’s possible to get a mortgage with a smaller down payment, 20 percent is a magic number, because you don’t have to pay for private mortgage insurance on top of your mortgage payment. Anika Hedstrom, MBA and senior financial analyst practicing in Medford, Oregon, also recommends putting down at least 20 percent because “a larger down payment decreases the total interest paid over the life of the loan.” But, the rule isn’t absolute and your personal circumstances may justify buying with a smaller down payment, she says. “There are locations where home prices are appreciating at a rapid rate,” says Hedstrom. “If waiting an additional couple of years to increase savings from 10 percent to 20 percent results in a much higher purchase price and higher interest rates, it may be best to forge ahead and purchase sooner. Ultimately, it’s your gamble and no one can predict with absolute certainty what will happen to interest rates and real estate appreciation.”

Budget for Acquisition Costs

The down payment isn’t the only thing you should be prepared to pay when you close on the home. “Typically, these are things like title insurance, title search, other government fees and escrow fees,” says Hedstrom. “In 2013, Bankrate.com estimated average closing costs of $2,402 for a $200,000 mortgage with a 20 percent down payment and excellent credit. This estimate includes lenders origination fees and third-party fees, but neglects the above-mentioned fees, making the total much larger.” According to Hedstrom, if possible it’s best to pay these fees in cash rather than rolling them into the mortgage, because you will end up paying interest on that money. Plus, it never hurts to ask the seller to pay. According to Hedstrom, “Some first-time buyers may get the seller to pay some or all of these fees.”

Budget for Additional Costs

Budgeting to buy your first house shouldn’t stop with making sure you have a sufficient down payment and can squeeze the mortgage payments into your monthly budget. Hedstrom points to the words of Robert Shiller, a Yale economist, who reminds home buyers that housing takes maintenance, depreciates, and goes out of style. Hedstrom also cautions that “homeowners forget about phantom costs of owning a house… including property taxes, homeowners insurance, umbrella policies, lack of liquidity and opportunity costs.” Taking these additional costs of owning versus renting into consideration before you buy helps ensure you’re able to happily afford your new home.

Focus on Big Wins

While every dollar counts, focusing on line items in your budget that can result in big savings can help you build up the cash to be in a position to buy a home sooner. Hedstrom calls these types of items “big wins” and explains that “Instead of cutting out lattes, review your budget and identify two to three of your largest monthly expenses. For some, this can be eating out and entertainment; for others this could be cable and technology/electronics.” Once you’ve identified your big wins, Hedstrom suggests cutting a fraction of the costs every week and deposit the money into a separate account.

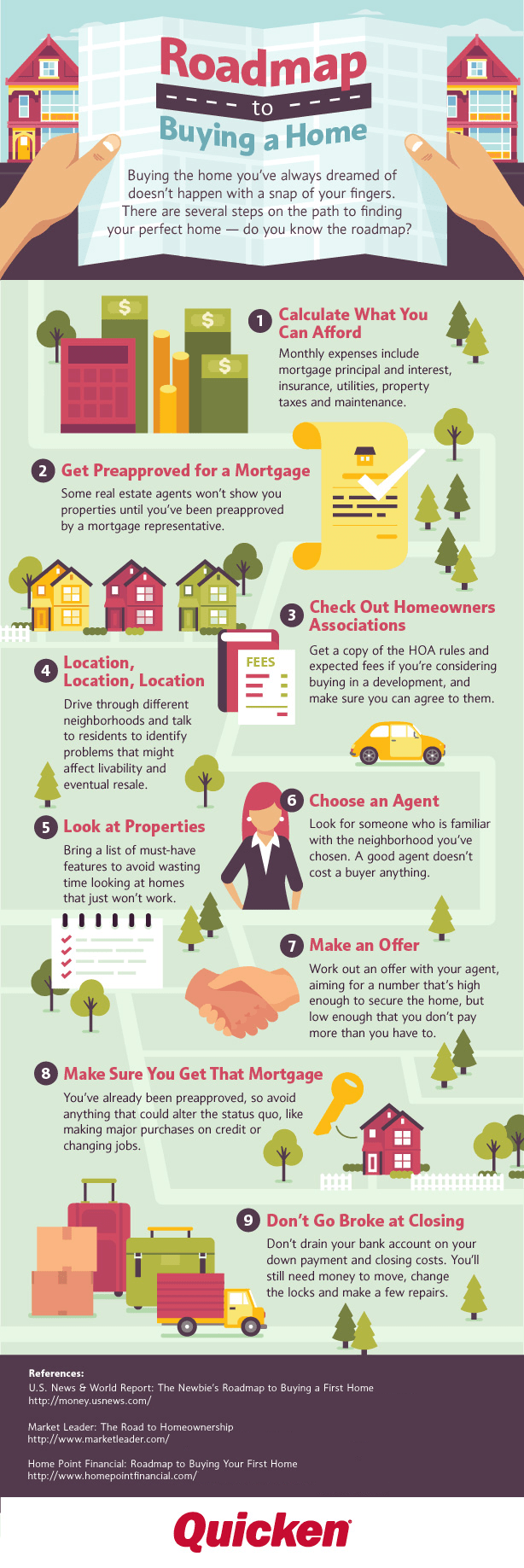

Click image to see full infographic

Quicken has made the material on this blog available for informational purposes only. Use of this website constitutes agreement to our Terms of Use and Privacy Policy. Quicken does not offer advisory or brokerage services, does not recommend the purchase or sale of any particular securities or other investments, and does not offer tax advice. For any such advice, please consult a professional.

{kind=link}

{kind=link}

{kind=link}