Comprehensive financial management, simplified.

Get all the information you need, right when you need it, to make the best choices for your money.

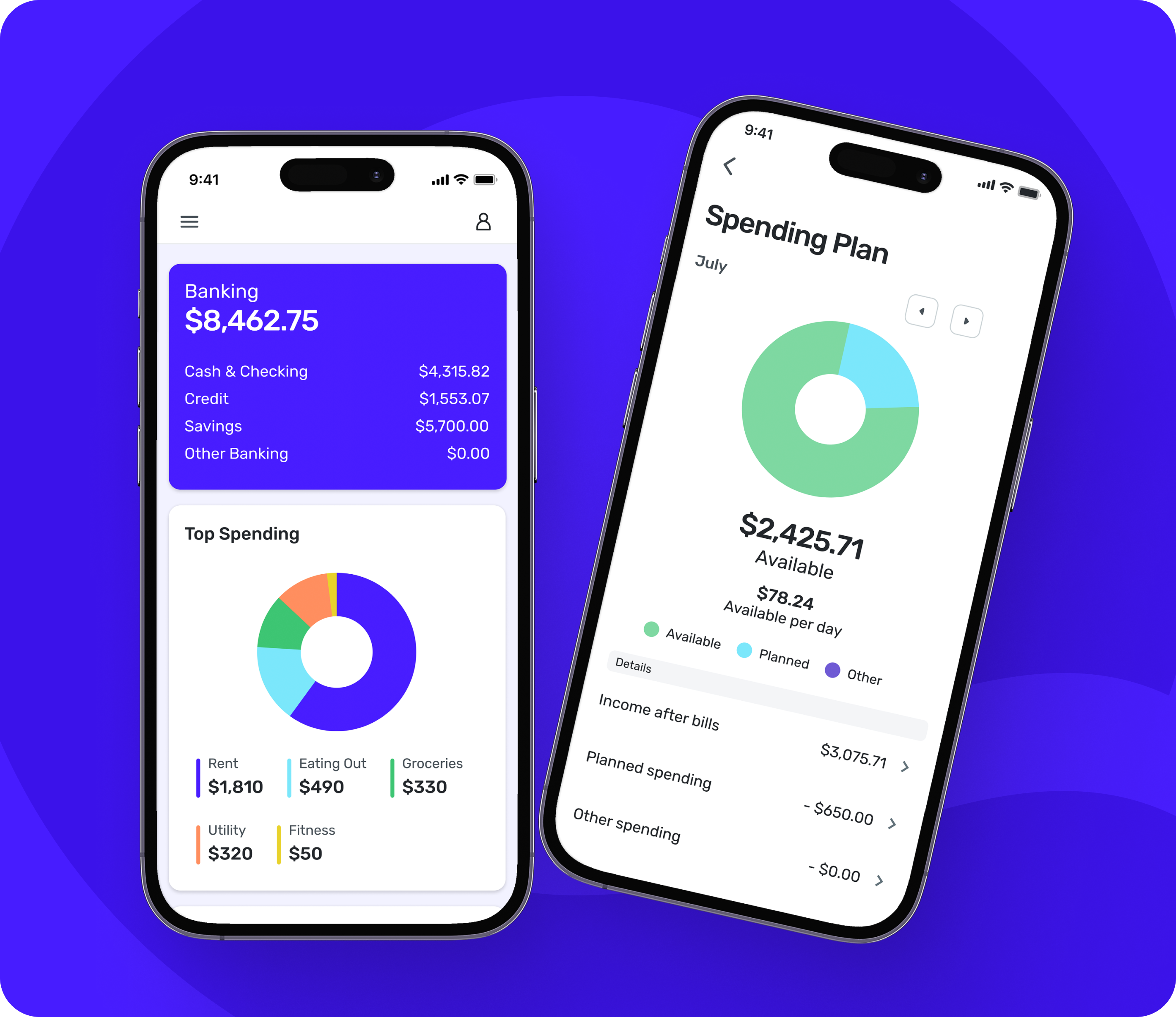

Connect all your financial accounts

Get a better budget & save more money

Customize your financial views

Get started on your own or with an expert

All Quicken plans

Find the right plan for your financial goals

Select the best fit for your finances

Quicken Simplifi

Mobile

Web app

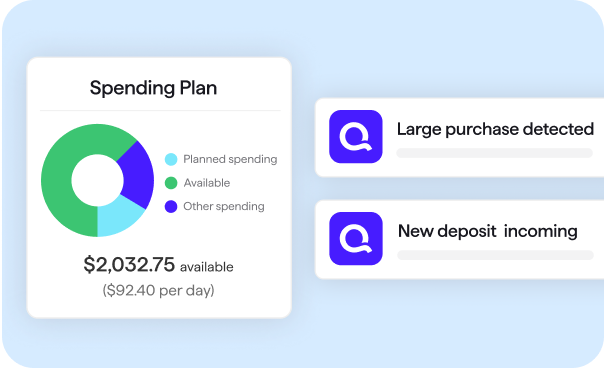

Save more money

Save more money- Always know what you have left to spend or save

- Get insights with real time alerts & reports

- Customize your transactions

Quicken Classic Premier

Mac

Windows

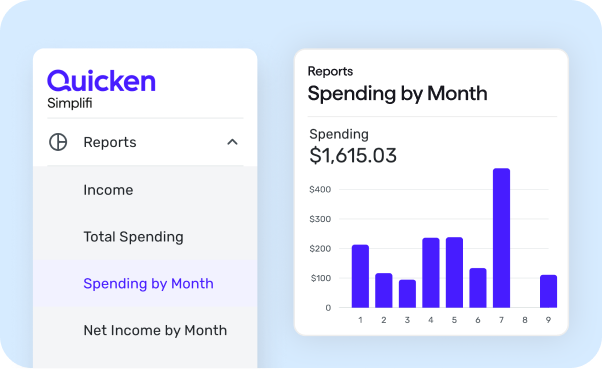

Best-in-class investing tools

Best-in-class investing tools- Built-in tax reports

- Reconcile to the penny

- Track & pay bills in Quicken

- Set budgets, manage debt, create a retirement plan

Quicken Classic Business & Personal

Windows

Mac

- Manage business, rental & personal finances

- Optimize for taxes

- Keep documents organized

- Reports: P&L, cash flow, tax schedules, and much more

“

“Worth its weight in gold -- seriously, worth so much more than I paid for it. I don't know what I would do without Quicken.

”Stan

- “

With [Quicken] Simplifi, I open my phone and I know in 5 minutes if I can afford the expensive item I want or I should hold off to next month or buy something cheaper.

” - “

Quicken is a useful, potentially life-changing tool that helps people take a confusing array of data and present it so that people can make important decisions in their life.

” - “

[Quicken] Simplifi gives us a clean, clear, concise picture of our monthly personal finances.

” - “

Quicken is the heart and soul of our household budgeting, planning and spending and will remain so as we age.

”Eddie

- “

I wanted a modern experience for managing my finances. [Quicken] Simplifi had a great user experience, and with the backing of Quicken, it was clear it would continue to be enhanced and improved.

”

Over 20 million better financial lives built, and counting

Trusted for over 40 years

#1 best-selling with 20+ million customers over 4 decades.Bank-grade security

We protect your data with industry-standard 256-bit encryption.